- When it comes to Part B (outpatient care) and Part D (prescription drug coverage) you may encounter some surprise premium costs.

- Roughly 7% (4.3 million) of Medicare enrollees pay more than the standard premiums for Parts B and D due to so-called income-related monthly adjustment amounts, or IRMAAs.

- Late-enrollment penalties may also apply in some situations for Parts B and/or D.

For some Medicare beneficiaries, health-care coverage ends up costing more than it does for most of their peers — and it's not by choice.

While there are costs that individuals often are aware of — i.e., they purchase a supplemental policy or choose a more expensive plan — some premium-related expenses sneak up on enrollees. And depending on the person, they could add up to thousands of dollars extra a year.

Roughly 62.6 million people — the majority of whom are age 65 or older — are enrolled in Medicare. Most pay no premium for Part A (hospital coverage) because they have at least a 10-year work history of paying into the system through payroll taxes.

Get South Florida local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC South Florida newsletters.

When it comes to Part B (outpatient care) and Part D (prescription drug coverage), however, you may encounter some surprise premium costs. And that can happen whether you stick with original Medicare (Parts A and B) or choose to get your benefits through an Advantage Plan (Part C).

Here's what to know.

Money Report

1. Higher premiums for higher income

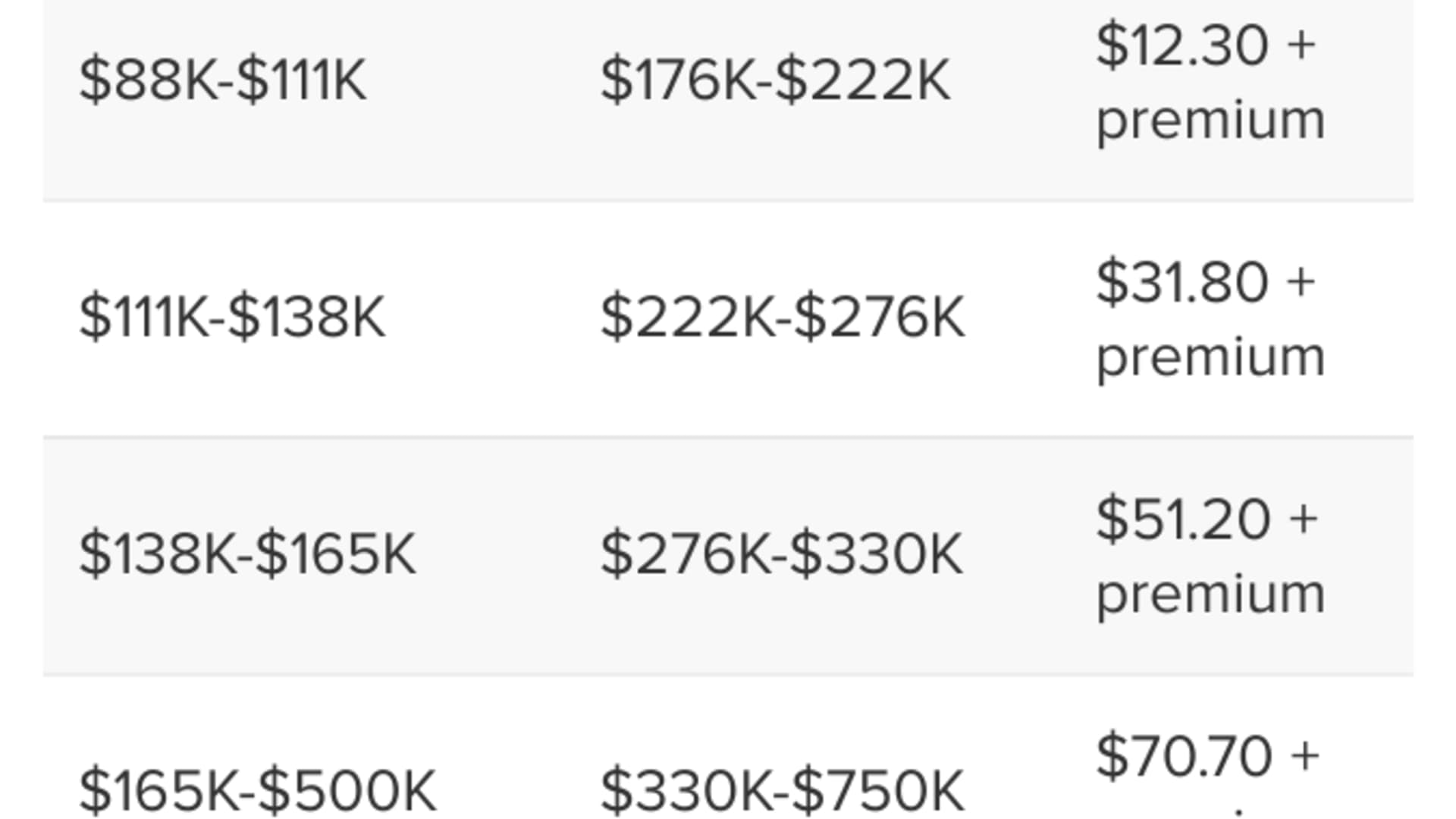

About 7% (4.3 million) of Medicare enrollees pay more than the standard premiums for Parts B and D due to so-called income-related monthly adjustment amounts, or IRMAAs, according to the Centers for Medicare and Medicaid Services.

Those amounts kick in at modified adjusted gross income of more than $88,000, and increase at higher income thresholds. For instance, a single taxpayer with income between $88,000 and $111,000 would pay an extra $59.40 per month for Part B on top of the standard premium of $148.50, or $207.90 total. (See charts below.)

And the IRMAAs don't gently phase in within each income bracket: Earn a dollar above the income thresholds, and the surcharge applies in full force.

"Many beneficiaries don't even know that Medicare costs anything at all," said Danielle Roberts, co-founder of insurance firm Boomer Benefits.

"So it adds insult to injury when they find out that not only do they have to pay for Medicare Parts B and D but also that they have to pay more than other people," Roberts said.

Generally speaking, the extra amounts are determined by your tax return from two years earlier.

You can ask the Social Security Administration to reconsider the surcharges if your income has dropped since that you filed that tax return.

You have to fill out a form and provide supporting documents. While it depends on your situation, suitable proof may include a more recent tax return, a letter from your former employer stating that you retired, more recent pay stubs or something similar showing that your income has dropped.

The required form includes a list of "life-changing" events that qualify as reasons for reducing or eliminating the IRMAAs, including marriage, death of a spouse, divorce, loss of pension or the fact that you stopped working or reduced your hours.

More from Personal Finance:

Early signs that you have a spending problem

How climate change is impacting retiree portfolios

How to choose an executor of your will

"Many of my clients have been able to get their IRMAA lowered due to a change in income because they retired and are no longer getting a paycheck," said Elizabeth Gavino, founder of Lewin & Gavino and an independent broker and general agent for Medicare plans.

If your request doesn't work, you can appeal the decision to an administrative law judge, although the process could take time and you'd continue paying those surcharges in the meantime.

2. Spousal income counts against you

Those IRMAAs also aren't just based on your own income. For example, if you have retired but your spouse is still working and your joint tax return shows modified adjusted gross income of $176,000 or higher, you would be subject to IRMAAs.

"This is why it's so important for people to begin educating themselves about Medicare a few years before they become eligible for it at age 65," Roberts said.

"Think about it – if you knew this at age 60, you might be able to consult with your financial advisor and do some planning to try to keep your modified adjusted gross household income below those thresholds," she said.

3. Sign up late, pay a penalty

Generally speaking, you're supposed to sign up for Medicare during a seven-month window that starts three months before your 65th birthday month and ends three months after it.

However, if you meet an exception — i.e., you or your spouse have qualifying group insurance at a company with 20 or more employees — you can put off enrolling.

Workers at those larger employers often sign up for Part A and delay Part B until they lose their other coverage. Then, they generally get eight months to enroll. The rules are different, though, for companies with fewer than 20 employees: Those workers are supposed to sign up when first eligible.

"Stop taking advice from friends and speak with the carriers or the HR departments to get confirmation on Part B requirements," Gavino advised.

For each full year that you should have been enrolled in Part B but were not, you could face paying 10% of the monthly Part B standard premium ($148.50 for 2021). The amount is tacked on to your monthly premium, generally for as long as you are enrolled in Medicare.

For Part D prescription drug coverage, the late-enrollment penalty is 1% of the monthly national base premium ($33.06 in 2021) for each full month that you should have had coverage but didn't. Like the Part B penalty, this amount also generally lasts as long as you have drug coverage.

"The part D [penalty] is the one that we see hit people most often," Roberts said.

"Although Part D is voluntary, if you don't enroll when you are first eligible and you don't have other creditable coverage ... you'll begin accumulating a penalty that grows larger with time," she said.