- The Consumer Financial Protection Bureau is expected to become a more aggressive consumer watchdog under the Biden administration.

- Consumer advocates say the bureau was almost entirely declawed under former president Donald Trump. Biden nominated Rohit Chopra, a former student loan official at the Obama-era agency, to head the CFPB.

- Likely focus areas include: Covid's financial impact, debt collection, student loans, payday loans, credit reporting, overdraft fees, racial equity and arbitration.

The Consumer Financial Protection Bureau is expected to become a more aggressive consumer watchdog under the Biden administration and while the coronavirus pandemic hurls financial challenges at millions of Americans.

Consumer advocates say the bureau was almost entirely declawed under former president Donald Trump, and during his tenure enforcement action steeply declined. The agency was created in 2010 after the previous economic downturn to protect people from predatory lenders.

Now, it's anticipated that the CFPB will more aggressively investigate consumer complaints and take action against companies that violate the law. To lead it, President Biden has nominated 38-year-old Rohit Chopra, a longtime consumer advocate and a former student loan ombudsman at the CFPB.

Of course, some were skeptical of the agency's work during the Obama administration, when Biden served as vice president. Mick Mulvaney, who served as Trump's acting CFPB director, at one time called the agency a "joke" in "a sick, sad kind of way."

But its work has never been more important, advocates say, as so many Americans try to rebuild their finances after almost a year of record job losses, evictions and increased debt. As people's money woes have increased, so have their issues with financial companies: Complaints to the CFPB were up 60% in 2020 from 2019.

Money Report

"There are potentially a dozen, two dozen priorities," said Richard Cordray, who served as CFPB director from 2012 to 2017. "There's a lot that needs to get done."

These are some of the likely focus areas for Biden's consumer watchdog.

Covid crisis

The Covid crisis will likely be the bureau's top priority, according to consumer experts and former agency officials.

The pandemic tipped the U.S. economy into the deepest recession since the Great Depression, and with historic speed. Millions of families were estimated to have slipped into poverty by year's end.

"Covid has created a new set of problems, or emphasized and underscored ongoing problems for consumers," Cordray said.

Americans may turn to financial firms for help, whether to seek various relief or new loans to cover expenses.

The CFPB will likely implement more safeguards to ensure consumers get adequate (and promised) support. That work will fall in two primary areas, said Patricia McCoy, a professor at Boston College Law School.

For one, the agency could ensure financial firms and debt collectors honor government protections, like the national ban on evictions until March and the payment pause for student loan borrowers through September. It may also uphold firms' voluntary commitments to all types of borrowers, like homeowners, car buyers and credit-card users, for example.

"That will be a top, top, top priority," said McCoy, a former agency official during the Obama administration.

Debt collection

In a similar vein, the agency will also likely try to overturn or rewrite Trump-era rules around debt collection, according to consumer advocates.

The prior administration issued two related rules toward the end of Trump's term, one in October and another in December. Broadly, they addressed how debt collectors may communicate with and disclose information to consumers.

Kathy Kraninger, the former CFPB head during the Trump administration, said the measures helped keep consumers informed. However, consumer advocates believe the rules gave companies too much power.

"At their core, these were not rules for consumers," said Rachel Gittleman, financial services manager at the Consumer Federation of America.

The Trump-era policies allow debt collectors to hound consumers by calling them one time per day, per debt, Gittleman said. A consumer with five medical bills could receive 35 calls a week, she said. There's also no limit on text or social-media messages.

The rules also don't prohibit the collection of "zombie debt," according to the National Consumer Law Center. Debts sometimes fall outside a statute of limitations for collection — but consumers may accidentally revive this time-barred debt by making a small payment, for example. That in turn frees up debt collectors to file lawsuits anew against a consumer.

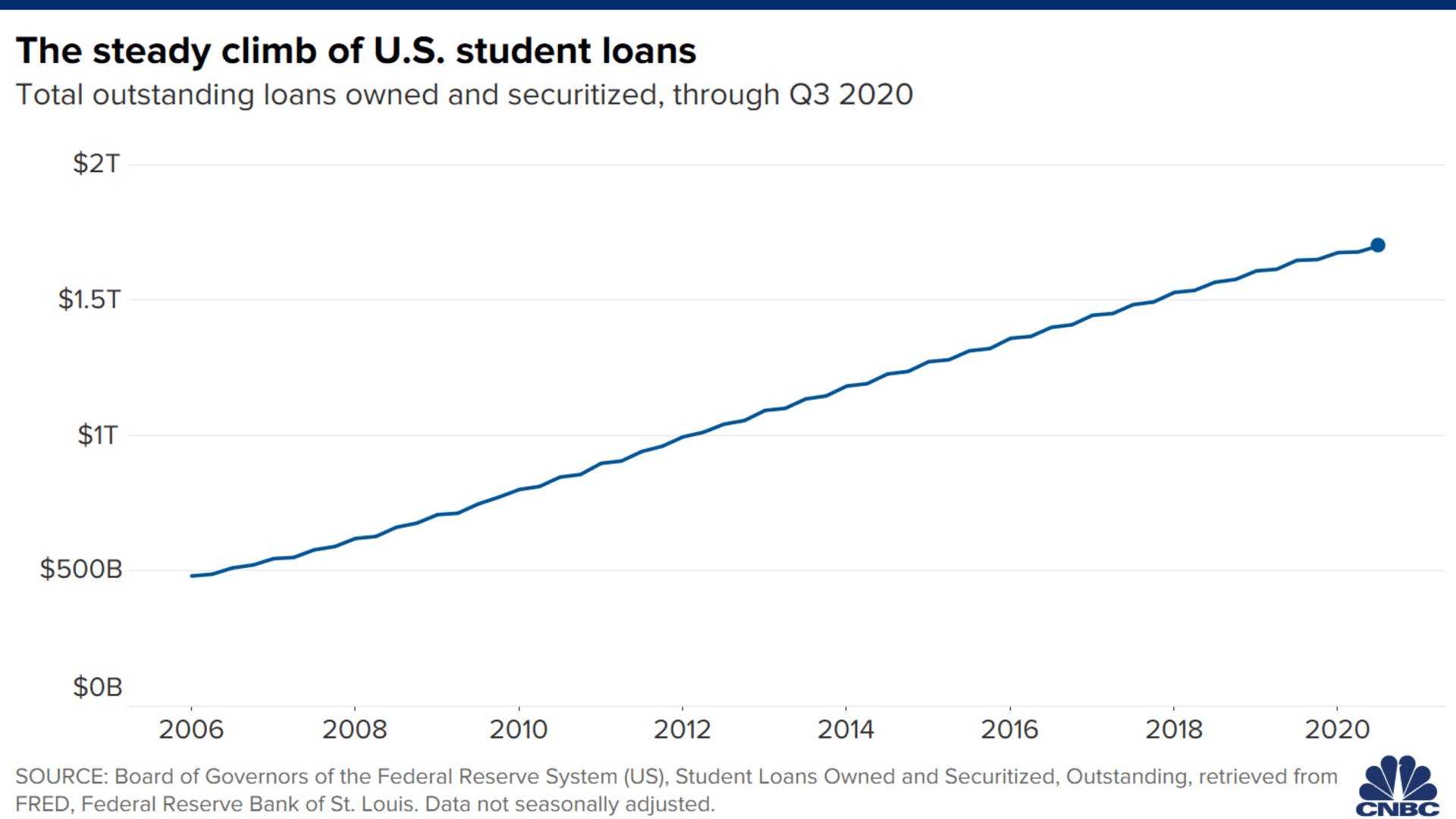

Student loans

Under Biden, the consumer bureau is expected to exercise greater enforcement of the rules on student loan servicing.

Advocates have criticized student loan servicers for misleading borrowers and steering them into more expensive repayment plans. During the Obama years, the bureau took legal action against Navient, one of the largest servicers. (Navient denies any wrongdoing.) With Biden in the White House, experts expect that lawsuit to be continued and pursued aggressively.

Other changes under Biden could include mandating that loan servicers tell borrowers about all of their available options, including economic hardship or unemployment deferments. And servicers that fail to do so could face penalties.

The consumer bureau will likely also take a harder stance against for-profit schools that have been known to prey on vulnerable students and make unrealistic promises. Enrollment at these schools usually increases in recessions, and it has during the pandemic.

"It is time for the CFPB to use all of its tools to stand up for student loan borrowers, including through enforcement actions, creating stronger protections, complaint monitoring and routine oversight of student loan companies," said Seth Frotman, executive director of the Student Borrower Protection Center, who worked at the bureau from 2011 to 2018.

Credit reporting

Credit scoring companies typically have to investigate consumer complaints within 30 days to 45 days. But the Trump administration's CFPB said it wouldn't take enforcement action against the companies if they take longer to do so during the pandemic.

That was the opposite of what the consumer agency should have done, advocates say. They anticipate Biden's CFPB will pressure the credit rating companies to respond quickly and adequately to people's complaints of false and outdated information on their records. These reports can determine the interest rate someone gets on a new car loan or mortgage or if they're accepted into an apartment.

It's clear people are running into challenges: More than half of the complaints that came into the CFPB between January 2020 and May 2020 were about credit reports.

Overdraft fees

In March, as the public health crisis caused unemployment to soar, federal regulators encouraged banks to waive their overdraft fees.

Instead, the average penalty has reached a record high of $33.47, a recent survey by Bankrate.com found. And checking account providers took in more than $30 billion in revenue from the fees alone in 2020, according to data provided to CNBC by financial research company Moebs Services.

When people are dinged with multiple fees, they can be pushed out of the banking system and find it impossible to receive stimulus aid like direct payments and unemployment checks, advocates say.

The CFPB should move to limit the charges, said Alex Horowitz, senior research office at Pew's Consumer Finance Project.

"It could restrict overdraft practices that it deems unfair, deceptive or abusive," he said. "An example might be a bank charging a customer many overdraft fees in a single day if a customer used a debit card several times."

Payday loans

Some 12 million Americans take out a payday loan each year. These loans carry extremely high interest rates for consumers — locking some in a vicious cycle of debt.

Last year, the Trump administration rescinded parts of a 2017 rule issued by Cordray, the CFPB head under President Obama, that sought to rein in potentially harmful payday-loan practices.

For example, the measure removed mandatory underwriting provisions (which had yet to take effect) that would have prohibited lenders from issuing money to consumers without first assessing their ability to repay the loan.

"I'd be shocked if the CFPB didn't get rid of that," McCoy, the former agency official, said of that measure.

Mandatory arbitration

Mandatory arbitration is a practice in which businesses require their employees and consumers to agree to arbitrate any possible legal disputes, rather than go to court or bring class action lawsuits.

The clauses have appeared over time in more and more contracts by credit card companies, banks, lenders and other businesses.

Advocates criticize the agreements, saying arbitration robs consumers of their day in court and allows companies to keep their wrongdoing secret because the proceedings aren't available to the public as they are with a lawsuit.

More from Personal Finance:

How Biden's $1.9 trillion relief plan would avert a looming benefits cliff

One year after Covid in America: A financial snapshot

What to know if you still haven't received your $600 stimulus check

"It really is a scandal in the house of justice, happening in broad daylight," said Cliff Palefsky, a San Francisco employment attorney.

The CFPB under Obama banned mandatory arbitration clauses in financial contracts, but the Trump administration overturned that rule. Now another reversal is possible.

"They can go a long way to protecting consumers in financial transactions and I suspect they will," Palefsky said.

Racial equity

All these efforts should be designed with an understanding that Black and Brown Americans have paid the biggest price for bad financial products and discriminatory lending, advocates say.

For example, the Center for Responsible lending has found payday lenders concentrate in African-American neighborhoods. Professors at the Massachusetts Institute of Technology, meanwhile, recently argued that a "Black tax" exists for African-Americans homeowners. And so on.

The previous administration didn't work to address these disparities, advocates say.

To the contrary, research shows that complaints to the CFPB from White, wealthy neighborhoods during the Trump era were far more likely to result in financial restitution for consumers than those that came in from low-income, Black neighborhoods.

When companies aren't penalized for their bad behavior, it just continues, said Remington Gregg, counsel for civil justice and consumer rights at Public Citizen.

"They banked on the CFPB not going after them," Gregg said. "We have to have robust enforcement of our laws."